Alberta Power Market Snapshot: April 2026

Shoulder season is here, and it exceeds even our already-high expectations for new power market records. Here is our 5-minute summary.

This article is for general informational purposes only and does not constitute financial, investment, or professional advice. Information is subject to change without notice and should not be relied upon for decision-making.

© 2026 Arder Energy™. All rights reserved.See Webpage Terms of Use.

The Data

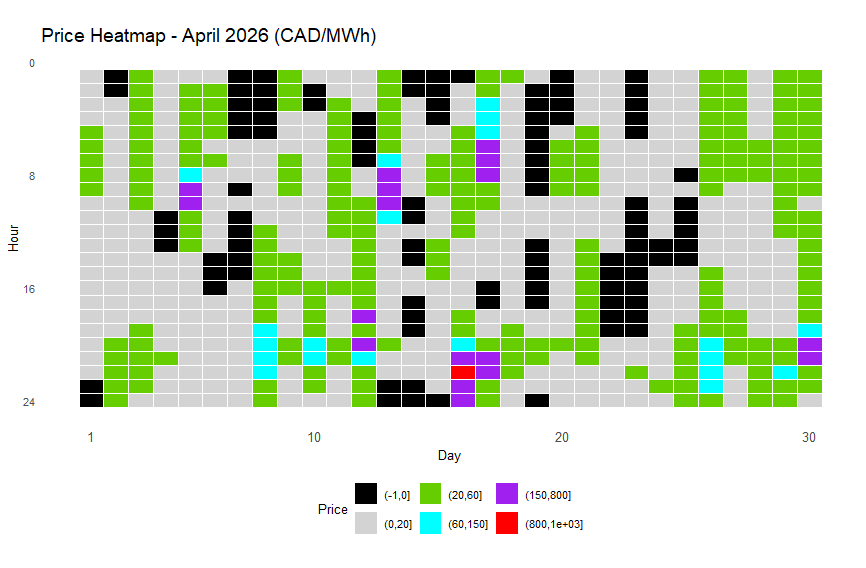

Let’s start with the heatmap - overall muted, with some more color but also large chunks of black - the zero-dollar price floor:

Heat Map of April 2026 hourly Alberta power pool prices

Black: zero dollar hour - “Excess Supply”

Light Grey: CAD 0.01 - 20/MWh - “Insufficient”

Green: CAD 20.01 - 60/MWh - “Marginal”

Cyan: CAD 60.01 - 150/MWh - “Full-cycle”

Purple: CAD 150.01 - 800/MWh - “Expensive”

Red: CAD 800.01 - 999.99/MWh - “Peak”

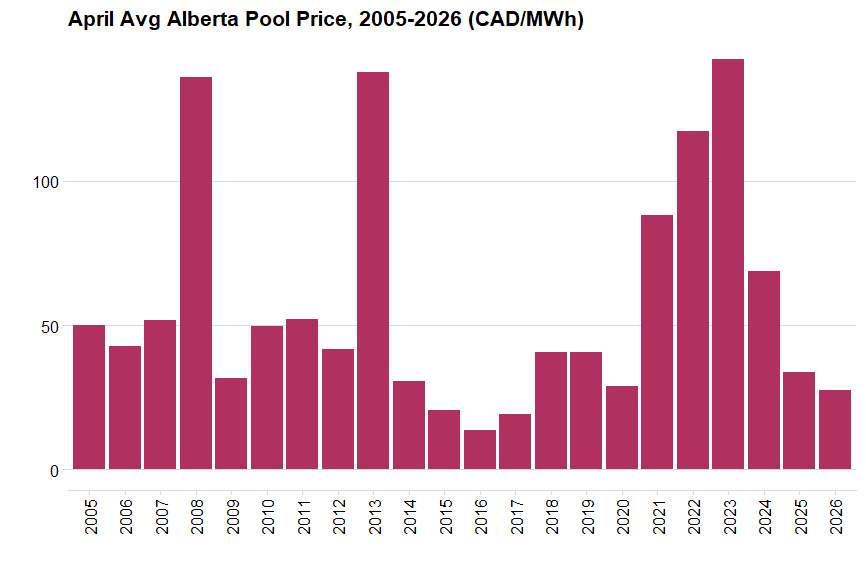

The average monthly pool price settled at CAD 27.61/MWh—8% lower than last April and the fourth-lowest average for the month since 2005. While these levels are well below the full-cycle recovery costs for any generator, a dip is expected during the "shoulder season." Limited heating and cooling demand, combined with BC’s significant hydro exports during the spring freshet, typically keep spring prices at their annual floor.

April average Alberta electricity pool prices, 2005-2026 (CAD/MWh)

Prices are not inflation-adjusted

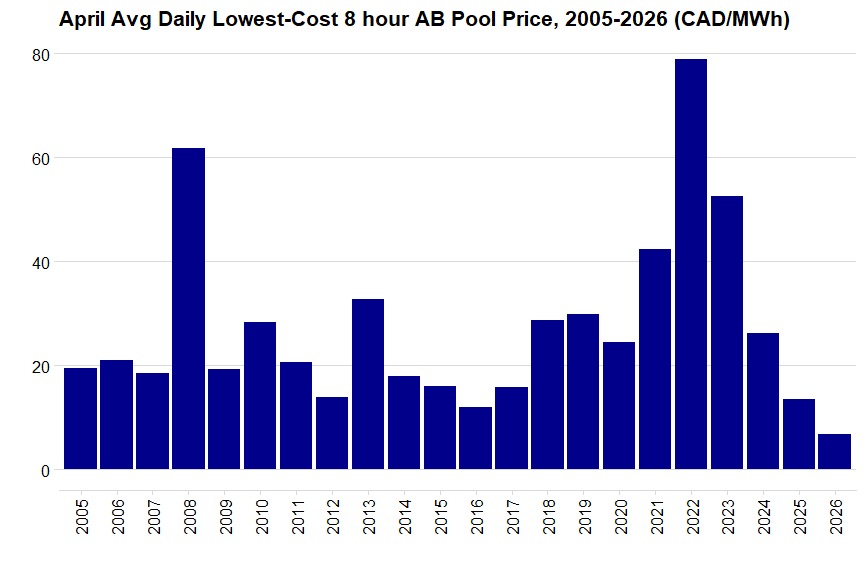

The real story, however, emerges when we look at the average price of the eight lowest-cost hours each day—our proxy for highly flexible loads. This average plummeted to CAD 6.79/MWh. This is not just the lowest April on record in over two decades; it is the second-lowest level for any single month since January 2005, trailing only the all-time low of CAD 6.36/MWh set in September 2024.

Daily lowest-cost 8 hours, average for April, 2005-2026 (CAD/MWh)

Prices are not inflation-adjusted

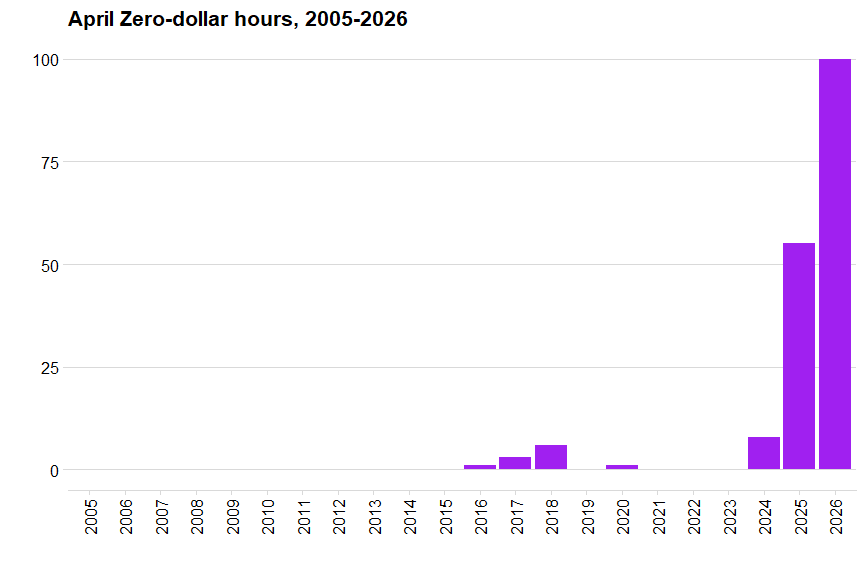

What is driving this collapse? The usual culprit: a record-breaking frequency of zero-dollar hours. We saw exactly 100 zero-dollar hours this month (13.9% of all hours). That is an 82% increase over last year:

Monthly zero-dollar hours for April, 2005-2026

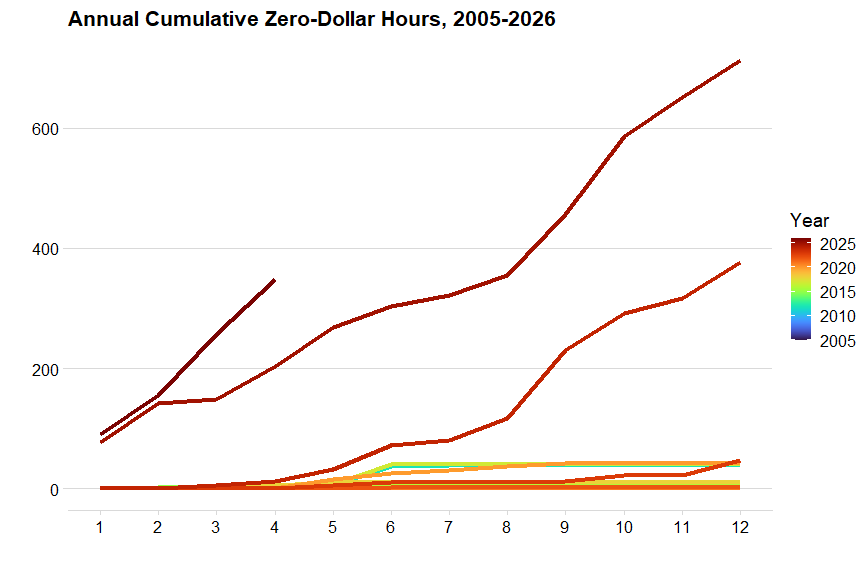

And year to date, by the end of April, we reached 356 zero-dollar hours. We are currently just 10 hours behind the pace of 2024’s then-record, having already hit 50% of last year's total volume (the all-time record) in just four months:

Annual cumulative Zero-Dollar Hours, 2005-2026

The Outlook

A frequent question, that we again received in our recent webinar, is whether this trend is sustainable. In short: zero-dollar hours could grow significantly more. Alberta’s current mix of inflexible gas-fired cogeneration, growing intermittent wind and solar, and limited intertie capacity creates a "perfect storm" for intermittent oversupply. The word “intermittent” here is key - we already see sharp price spikes during the evening load ramp especially when solar and wind power generation fall sharply. Thus for inflexible loads, the increase in zero-dollar hours often comes during the “wrong” hours.

And average prices below full-cycle costs create a much larger structural problem: when generators lack the incentive to invest in new capacity, we risk a supply gap despite massive projected load growth. This only increases the likelihood of future price spikes akin to the volatility we saw from 2021 to 2023.

To materially shift this trajectory, we need progress on four fronts:

More Flexible Load: While some industrial players already curtail consumption during price spikes, there is growing interest in using "downward flexibility" as a cost lever. Unfortunately, residential and small-business participation remains hamstrung by the delayed rollout of the Advanced Metering Infrastructure (AMI).

More Storage: Alberta lags significantly behind markets like Texas (ERCOT) in battery deployment. The primary bottleneck has been the lack of a competitive storage tariff, though this is currently under review and represents a massive opportunity for the province.

Improved Interties: Stronger interties would allow Alberta to export excess inflexible generation to neighboring provinces that are increasingly energy-short. The Alberta-Federal MOU is discussing expanded interties, with which Alberta would be well-positioned to become a cost-effective regional energy hub. [NOTE: In an earlier version of this article, we indicated that the AESO’s FFR+ procurement in 2026 would contribute to expanded export capacity; however, the program is primarily focused on increasing import capacity. Our thanks to Leonardo Tovar at the AESO for providing this clarification.]

Stronger Flexibility Incentives: Structural changes are coming via the Restructured Energy Market (REM). Shorter settlement intervals, Locational Marginal Pricing (LMP), and the new R30 ramping product—alongside ongoing Tariff Redesign—will finally put a proper price on flexibility.

The Bottom Line: These structural fixes will take time to materialize. In the meantime, expect us to keep sounding like broken records as we announce new zero-dollar records in the months to come.

Transforming Power into Competitive Advantage

The strength of Alberta’s power market lies in the agency it affords industrial participants. Through a combination of contractual, operational, and investment-based levers, organizations can transform power from a volatile cost center into a source of competitive advantage and resilience. If you are interested in exploring these strategies, please get in touch!

📊 ArderInsights Platform: From Market Metrics to Operational Strategy

Good strategies require good data. The ArderInsights Platform translates complex Alberta power metrics into operational realities, providing industry and investors with foundational market intelligence.

📈 1. Free & Premium Market Dashboards

Free Dashboard: Live tracking of Alberta Power Market pricing, zero-dollar hour frequency, and load dynamics.

Premium Dashboard: Advanced tracking of price, load and flexibility metrics, with optional private data integration.

📋 2. Regular Market Reports

Detailed monthly reports featuring price distributions, load flexibility, and TB2/TB4 arbitrage analytics, delivered promptly after month-end, available to Members through our platform.

🎓 3. On-Demand Training

Foundational capacity-building online training modules designed to establish a solid baseline across technical, commercial and regulatory power market aspects, available to Members through our platform.