Structural Market Change: Highlights from the MSA

Superb information on Alberta’s power market comes from the Market Surveillance Administrator (MSA), the province’s regulator, specifically through its quarterly reports. At nearly 100 pages of statistics, event descriptions, and interpretations, these reports provide deep insight into market dynamics and emerging trends.

The recently released Q4 2025 Wholesale Market Report certainly did not disappoint. However, as working through these details can be prohibitively time-consuming, here is our summary of the three findings we found most insightful and what they mean for industrial power consumers.

This article is for general informational purposes only and does not constitute financial, investment, or professional advice. Information is subject to change without notice and should not be relied upon for decision-making.

© 2026 Arder Energy™. All rights reserved.See Webpage Terms of Use.

Prices - An Interim Low?

For anyone following our blog series this won’t be news, but given the significance to power consumers it is worth reiterating: average electric energy prices have fallen sharply over the past three years in Alberta. As the MSA highlights:

“The lower pool prices in 2025 were driven by increased gas generation from Cascade and Base Plant, in addition to more wind and solar (intermittent) generation. This additional supply offset higher demand, more exports, a higher carbon price, and higher natural gas prices year-over-year.”

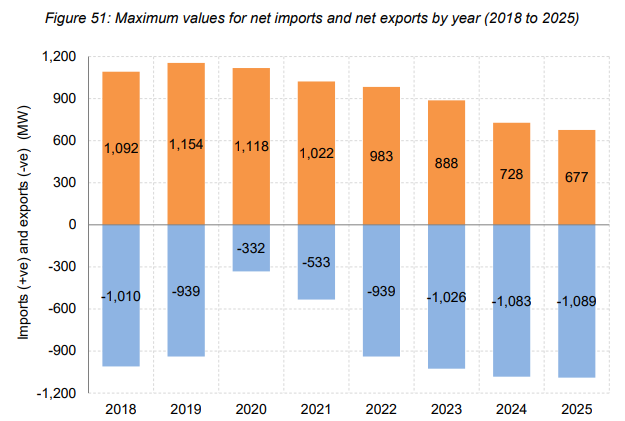

On top of that, Alberta has become a significant power exporter:

“In 2025, Alberta exported a record 348 MW on average, compared to exports of 212 MW in 2024. Historically, Alberta has been an importer of power, with higher prices than in other jurisdictions. This has shifted in recent years. In 2025, pool prices in Alberta were below real-time prices in Northern California 77% of the time.”

Alberta Power Market, Net Imports and Net Exports by year (2018 to 2025)

Source: MSA Alberta, Wholesale Market Report Q4 2025, p.65

But these low prices may not be sustainable. The MSA’s net revenue analysis makes this point abundantly clear: even at a modest 6.5% Weighted Average Cost of Capital (WACC), 2025 pool prices were insufficient for cost recovery across all major technologies—combined-cycle, simple-cycle, wind, and solar alike. While many assets have different commercial structures, the takeaway is clear: current spot levels are structurally unsustainable for the long-term economic viability of the supply stack.

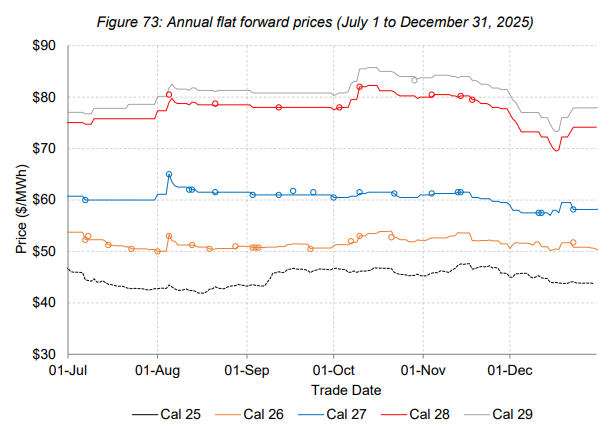

Significant amounts of new load are also waiting in the queue (see “Alberta Power: GROWTH!”). Accordingly, forward prices remain elevated, with calendar years 2028 and 2029 closing at CAD 74.19/MWh and CAD 77.94/MWh respectively on Dec 31st:

Annual Forward Prices, Alberta Power Market, Q4 2025 Pricing

Source: MSA Alberta, Wholesale Market Report Q4 2025, p.88

This compares to an actual average price of CAD 43.68/MWh for 2025. While forward prices are never perfect predictors, they point to significant price pressures.

The Zero-Dollar Era

Another structural shift we are tracking closely is the accelerating frequency of zero-priced power. The latest MSA data confirms that the System Marginal Price (SMP) was at CAD 0/MWh for 10.6% of all minutes in 2025.

That number is higher than the 8.1% of all hours that cleared at zero (see “Alberta Power: 2025 in Review“) because the SMP is determined every minute, but pool prices settle in hourly increments. If prices are different from zero for just one minute, that hour will not clear at zero. Notably, a key feature of the Restructured Energy Market (REM) coming in 2028 is 5-minute settlements. In a market hitting zero one-tenth of the time, these shorter intervals will provide a further incentive for loads to behave flexibly.

A Tale of Two Peaks: Structural Decoupling

On December 11, 2025, Alberta hit a new hourly all-time demand record of 12,785 MW. In years past, a peak of this magnitude—set during an evening hour with zero solar and -22°C temperatures—would have been a guaranteed recipe for triple-digit scarcity pricing.

We saw the "old" reality on January 11, 2024, when a lower peak shot the pool price up to CAD 629/MWh. This time, the market did not even flinch. Despite the record load, the price averaged a remarkably quiet CAD 44/MWh.

This is no anomaly; it is a symptom of a structural shift. The massive baseload injection from the new Cascade Combined Cycle and Suncor Base Plant Cogen units, paired with ~2 GW of wind producing throughout the peak, has fundamentally changed the supply stack. We are seeing a clean decoupling between demand and price. For anyone still hedging based on the historical "winter peak = expensive power" playbook, the December 11 event is a clear warning: those correlations are structurally broken.

Key Takeaway

This Q4 2025 report makes one thing clear: Alberta’s power market transformation is structural, not cyclical. Industrial players who proactively adapt to these shifts will secure more resilient, cost-competitive power than peers clinging to the outdated "set and forget" procurement model. And the current “calm before the storm” is the right time to review and update power strategies.

Sign up for our free Webinar on April 16th

We will break down these developments in an upcoming free, 30-minute webinar—covering market records, the REM timeline, and specific strategies for industrial loads—while reserving time for your questions.

Date: April 16th, 11-11.30am MT

Sign up here →https://arder.ca/webinars