LNG Shut-ins? Don’t count on it.

An unprecedented build-out of LNG capacity is under way - global liquefaction capacity is poised to increase by over 50% by the end of the decade. Spot prices are starting to recede, US Henry Hub spot prices have increased sharply. And over the past couple of weeks, a number of articles received a lot of attention suggesting that US LNG production may be forced to shut in within the next few years as margins compress.

Don't count on it - here is why, and what that means for market participants.

[This article is not financial or investment advice, but provided for general information purposes only. All information is subject to change and should not be relied upon for any decision making. Copyright 2025 Arder Energy™. All rights reserved. See Webpage Terms of Use.]

The Questions

Here are the three questions that have surfaced most frequently in recent weeks:

At what Marginal Spreads will US LNG capacity shut in as margins compress?

Do current forward curves already point to such a scenario in the near term?

What does this mean for market participants?

The TL;DR:

Somewhere around 15% of Henry Hub plus USD 2/MMBtu - or less.

No.

Don’t rely on Shut-Ins to keep spot prices elevated.

As usual though, it’s worth diving into the details.

Let's go!

Pricing Formulas and Economics

The vast majority of long-term US LNG Sale & Purchase Agreements (SPAs) are based on one of three general pricing arrangements:

Tolling: A "cost-plus" formula, typically expressed as: Price(LNG) = 115%*Henry Hub (Beta) + x (Alpha)

Spot: Europe’s physically-settled Title Transfer Facility (TTF) and JKM (Japan Korea Marker) serve as primary global price proxies (see “JKM: Top 3 Considerations for Deal Leads“ for more details)

Netback: A spot price indexed formula, generally calculated as a percentage of TTF or JKM minus certain fixed and variable costs (e.g., shipping, regasification).

[Note that the "classic" type of LNG pricing formula—crude-indexing—remains non-typical for US-origin LNG cargoes due to the separation of US gas from global crude markets.]

We exclude Netback agreements from this review: these typically obligate the seller to provide cargoes regardless of price levels, and the buyer generally lacks the incentive to cancel cargoes unless severe physical demand destruction (e.g., a major recession) occurs. In other words, Netback volumes will generally keep flowing regardless of price levels.

Take-or-Pay (TOP) Obligation

For Tolling agreements, the Alpha (Liquefaction Fee) forms the definitive Take-or-Pay (TOP) obligation for the buyer. Whether or not the buyer takes the physical cargo, they must pay this fixed amount for the agreed minimum contract quantity. This is the entire function of a tolling agreement: to allow the facility operator to recover the capital investment and achieve the required rate of return via a fixed, long-term charge. The Alpha is thus a sunk cost and irrelevant to the buyer’s immediate, marginal decision-making.

The Beta, defined as 115% of Henry Hub, approximates the cost of the feed gas plus the fuel gas consumed in the liquefaction process. When a cargo is cancelled, the buyer remains responsible for the cost of the feed gas. Because the gas was never consumed, the buyer (or the facility on the buyer's behalf) can resell the feed gas back into the market. The key assumption is that with sufficient notice, the buyer can substantially mitigate the feed gas cost through resale, incurring only basis risk and minor transactional costs.

Marginal Spreads

As most US cargoes are currently directed toward Europe, and the TTF and JKM prices are highly correlated, we focus our incremental analysis on the TTF market.

To move the gas to the European destination hub (TTF), the buyer incurs two primary marginal costs:

Shipping: Transportation to a European port costs somewhere around USD 1-1.5/MMBtu at mid-market shipping rates (Note: Shipping rates are highly volatile, thus this number can vary substantially - tread with caution).

Regasification & Grid Access: The LNG must be regasified and injected onto the Dutch gas grid. We will use the recent Platts Northwest Europe Market to TTF basis of approximately USD 0.5/MMBtu as a cost proxy for this step.

Thus, the forward-looking marginal cost for a European LNG buyer under a long-term US tolling SPA is the variable cost of the gas plus the transport costs: 115%HH + Shipping + Regasification, or 115%*HH + ~USD 2/MMBtu.

To determine the marginal spread that incentivizes a cargo uplift, we are concerned with the price difference between TTF and HH. We therefore deduct the Henry Hub price:

Marginal Spread = Marginal Cost to TTF - HH

= 115%*HH + ~USD 2/MMBtu - HH

= 15%*HH + ~USD 2/MMBtu

In other words, under this approximation TTF needs to be higher than HH by at least 15% of HH plus ~USD 2/MMBtu for LNG to keep flowing.

Forward Prices

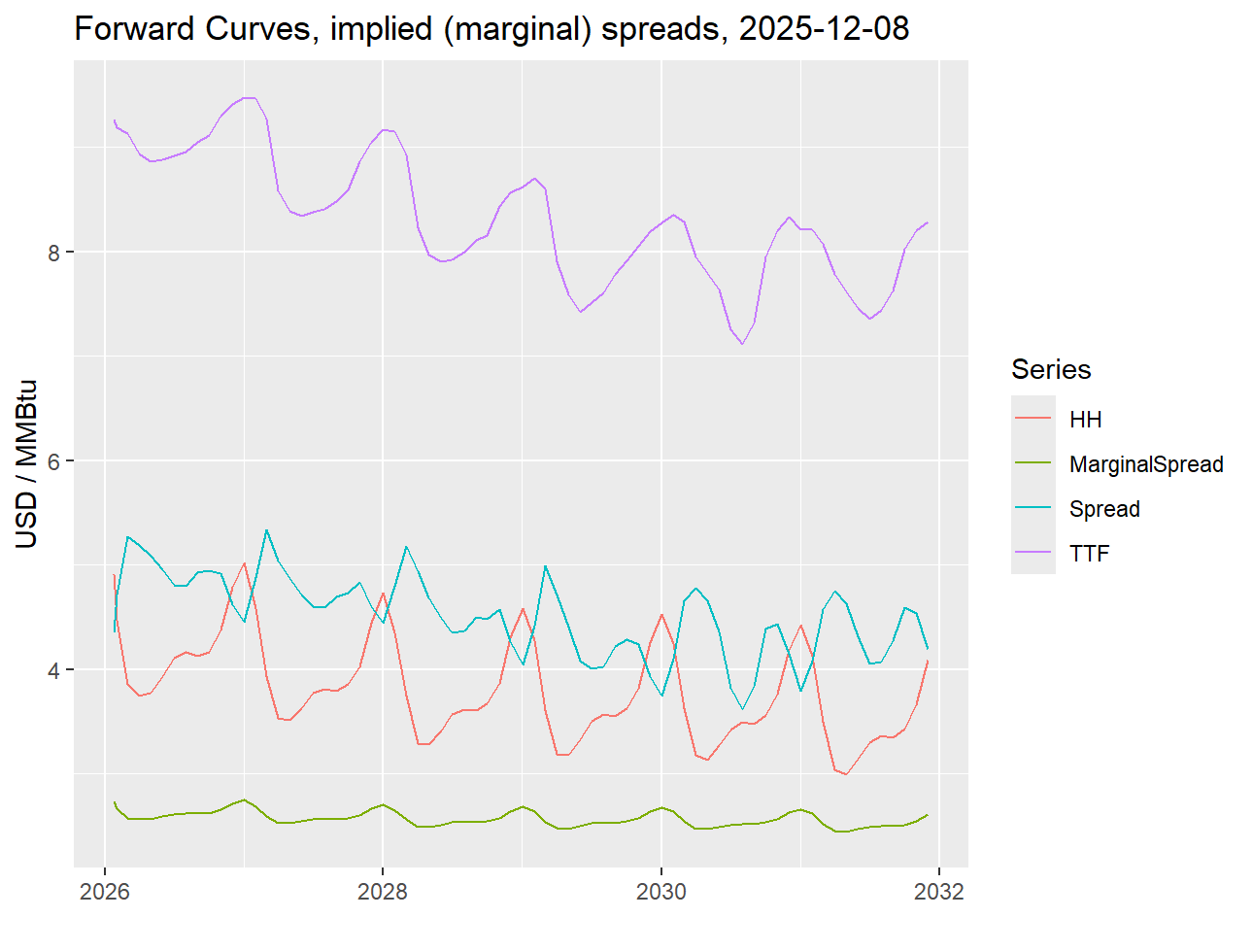

Front month TTF today (Dec 8, 2025) is just over USD 9.30/MMBtu, with HH at just under USD 5/MMBtu for a spread of ~USD 4.3/MMBtu and a Marginal Spread of USD 2.75/MMBtu. In other words, the spread could reduce by another ~USD 1.6/MMBtu before we should see any capacity shut-ins.

A look at the forward curve confirms this structural resilience. Even in June 2029, where TTF trades at ~ USD 7.50/MMBtu HH at ~ USD 3.30/MMBtu, the outright spread remains strong at over USD 4/MMBtu.

The below chart shows this clearly. The TTF-HH spread based on forward curves as of 08 December 2025 remains well above the implied Marginal Spread (calculated per the methodology outlined above, 15%HH + USD 2/MMBtu), throughout the next 7 years.

HH, TTF Forward Curves and implied (marginal) spreads

Capacity shut-ins are certainly possible, but they will require the market to fundamentally deviate from the current forward curve: specifically, the TTF-HH spread must compress significantly from current levels for a sustained period.

What this Means

The key takeaway for market participants is simple: ensure that your position is resilient against prolonged periods of tight spreads. DO NOT count on capacity shut-ins to keep spot prices elevated.

Conversely, manage your exposure to potential price spikes, whether they represent a fundamental risk to your margins or a structural opportunity for your portfolio.

No one truly knows what the next few years will bring, but the market is shifting at an unprecedented rate.

Buckle Up!

Limitations

Isn't it more complicated than that? Absolutely, and here are some of the key and limitations that complicate the analysis. Note however that none of them change the overall "high level" conclusion about marginal shut in cost levels - rather, they indicate likely time lags, a larger uncertainty range around threshold levels and "temporary exceptions to the rule".

Intransparency: The LNG Market is well known for the wide range of specific contract terms used in seemingly similar agreements. Two tolling agreements with the same headline terms may have vastly different quantity / flexibility terms. Thus some contracts may behave differently from what we would normally expect.

Liquidity: The presented analysis assumes that all counterparts remain sufficiently liquid to deliver on their contractual obligations. Should large counterparts become insolvent, then the resulting recontracting of volumes may change equations materially.

Marginal Shipping & Regasification costs: A significant part of shipping & regas costs, most likely in the short term, may also be sunk, thus the marginal cost of shipping & regas may be substantially lower than the estimated USD 2/MMBtu. This would allow for even deeper margin compression before shut-ins occur - don’t be too surprised if they only take place once spreads fall to around a dollar, especially if it appears as if the drop may be temporary.

Buyer commitments: Buyers may need to keep taking cargoes even below marginal break-even levels if they are unable to cancel or otherwise satisfy their downstream / back-to-back commitments.

The Big Unknown: Should high Henry Hub prices start impacting US inflation rates, will the US government consider export restriction? This may seem very unlikely right now, but crazier things have happened.

(These are some of the reasons why this article is for general informational purposes and it does not constitute financial, investment or other professional advice. It should not be used for decision making. We are transparent about our reasoning and the underlying assumptions so that you can come to your own conclusions.)

LNG Strategy Training for Deal Makers

This focused, in-person course is designed for key decision-makers who are actively involved in structuring, analyzing, and executing high-stakes LNG deals:

Deal Leads & Lawyers delivering complex LNG agreements

Executive & Board Members reviewing and designing long-term strategies

Financial Analysts, Insurance Professionals, and Government Regulators conducting project due diligence

Conducted in an interactive setting in Calgary, the session delivers the insights and expertise necessary for effective deal architecture and risk management:

Global LNG Market Dynamics

Economics & Pricing Formulas

Key Sale & Purchase Agreement Terms

Canadian LNG Value Chain Optimization

Top Mistakes to Avoid

Due to the small-group, peer-level format, capacity is limited to ensure maximum interaction and value.

We expect to sell out early again - sign up now!